The Mortgage That Looks Friendly… Until It Isn’t

At first glance, adjustable-rate mortgages feel like a gift.

Lower payments.

Easier approval.

More house for the same budget.

The numbers look kind.

The lender sounds reassuring.

The spreadsheet says “affordable.”

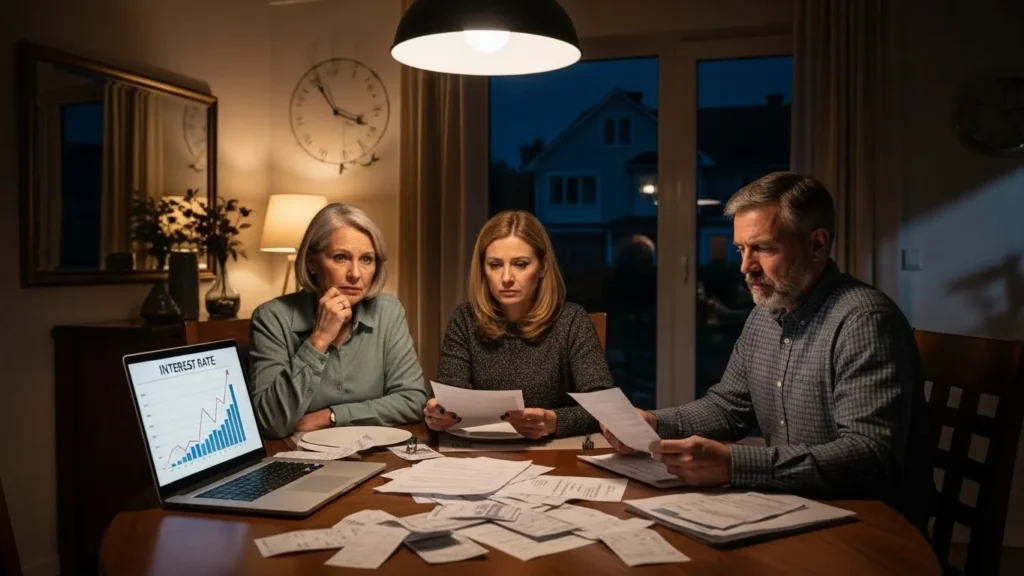

And then—years later—something changes.

A letter arrives.

Your interest rate adjusts.

Your monthly payment jumps.

Suddenly, the mortgage that felt manageable begins to feel heavy.

👉 This is the quiet risk of adjustable-rate mortgages (ARMs): they delay discomfort rather than eliminate it.

Understanding why ARMs can be risky doesn’t require advanced finance.

It requires understanding how uncertainty compounds over time.

What an Adjustable-Rate Mortgage Really Is (In Simple Terms)

An adjustable-rate mortgage has two phases:

- Introductory period – A fixed, usually low interest rate

- Adjustment period – The rate changes periodically based on market conditions

Common structures include:

- 5/1 ARM (fixed for 5 years, adjusts yearly)

- 7/1 ARM

- 10/1 ARM

During the first phase, ARMs often feel like a win.

Payments are lower than fixed-rate mortgages.

Cash flow feels easier.

The loan feels “smart.”

But the risk doesn’t live in the beginning.

It lives in what happens after.

The Core Risk: You Don’t Control the Future Rate

The biggest danger of an adjustable-rate mortgage is simple:

👉 Your future payment depends on factors you cannot control.

These include:

- Central bank interest rate changes

- Inflation trends

- Economic cycles

- Global financial events

Even if your loan has caps (limits on how much rates can rise), increases can still be significant.

A 2–3% jump in interest may sound small.

On a large mortgage, it isn’t.

Why Rising Payments Hurt More Than People Expect

Humans adapt quickly to “normal.”

When your ARM payment starts low, your lifestyle adjusts around it.

You:

- Commit to other expenses

- Build budgets assuming stability

- Make long-term plans

When payments rise, the shock isn’t just financial.

It’s emotional.

Suddenly:

- Saving becomes harder

- Flexibility disappears

- Stress increases quietly, month by month

This is why payment volatility matters more than spreadsheets suggest.

Adjustable vs Fixed: A Clear Risk Comparison

| Feature | Adjustable-Rate Mortgage | Fixed-Rate Mortgage |

|---|---|---|

| Initial Payment | Lower | Higher |

| Payment Stability | Low | Very high |

| Exposure to Rate Hikes | Yes | No |

| Long-Term Predictability | Weak | Strong |

| Budgeting Ease | Difficult | Easy |

| Stress During Rate Changes | High | Low |

ARMs aren’t bad by default — but they demand more vigilance and tolerance for uncertainty.

The Hidden ARM Details Many Buyers Miss

1. Rate Adjustment Frequency

Some ARMs adjust:

- Once a year

- Every six months

- Even monthly

More frequent adjustments = more uncertainty.

2. Rate Caps Aren’t Always Comforting

Most ARMs have:

- Initial caps (first adjustment)

- Periodic caps (each adjustment)

- Lifetime caps (maximum rate)

But even with caps, payments can rise sharply over time.

A “safe” cap still means higher payments.

3. Index + Margin Complexity

Your new rate isn’t random — it’s tied to:

- A benchmark index

- A lender margin

This complexity makes future payments hard to predict with confidence.

The Refinancing Myth: “I’ll Just Refinance Later”

This is one of the most dangerous assumptions in home finance.

Refinancing depends on:

- Interest rates at that time

- Your credit score

- Your income stability

- Property value

If any of these move against you, refinancing may not be possible — or affordable.

👉 ARMs are safest when they still work even if refinancing fails.

Most people don’t plan for that scenario.

Who Is Most at Risk With Adjustable-Rate Mortgages?

ARMs become especially risky for:

- First-time buyers without experience

- Households with tight budgets

- Buyers stretching to afford a home

- People with variable income

- Long-term homeowners

If rising payments would force painful lifestyle cuts, the risk is already too high.

When Adjustable-Rate Mortgages Can Make Sense

Despite the risks, ARMs aren’t universally wrong.

They may be reasonable if:

- You plan to move within the fixed period

- You have significant financial buffers

- Your income is expected to rise predictably

- You fully understand adjustment mechanics

The key difference: intentional planning vs hopeful assumptions.

Real-Life Example: The Payment Shock

Scenario:

- Home price: $450,000

- ARM starts at 3.5%

- Fixed alternative: 5.5%

At first, the ARM saves hundreds per month.

Five years later:

- Rates rise

- ARM adjusts to 6.5%

Monthly payment increases by a large margin.

Same house.

Same loan.

Different reality.

The problem wasn’t the math — it was the timeline.

Why This Matters More Than People Admit

Mortgage stress doesn’t arrive suddenly.

It builds quietly:

- Slightly tighter months

- Less saving

- More financial anxiety

Over time, it affects:

- Career choices

- Family decisions

- Mental peace

A mortgage should support your life — not dictate it.

That’s why understanding ARM risk matters beyond numbers.

Mistakes to Avoid With Adjustable-Rate Mortgages

❌ Choosing based only on the lowest payment

❌ Ignoring worst-case scenarios

❌ Assuming income growth will save you

❌ Underestimating emotional stress

❌ Failing to read adjustment terms carefully

Each mistake compounds the next.

Safer Alternatives to Consider

If you’re unsure about ARM risk:

- Fixed-rate mortgages offer clarity

- Shorter loan terms reduce exposure

- Conservative borrowing protects flexibility

Sometimes the “boring” option is the strongest one.

Key Takeaways

- Adjustable-rate mortgages shift risk into the future

- Low initial payments can hide long-term stress

- Rate adjustments depend on forces you can’t control

- Refinancing isn’t guaranteed

- ARMs require planning, buffers, and risk tolerance

- Stability often beats short-term savings

Frequently Asked Questions

1. Are adjustable-rate mortgages bad?

Not inherently, but they carry more risk than fixed-rate loans.

2. How much can ARM payments increase?

It depends on caps, loan size, and rate movements — but increases can be substantial.

3. Are ARMs good for first-time buyers?

Usually no, unless timelines and risks are clearly understood.

4. What’s the biggest ARM mistake?

Assuming refinancing will always be possible.

5. Is a fixed-rate mortgage safer?

Yes, in terms of predictability and long-term stability.

A Calm Conclusion

Adjustable-rate mortgages don’t fail because they’re complicated.

They fail because people underestimate how uncomfortable uncertainty can feel when it shows up monthly.

If your mortgage allows you to live calmly — even when conditions change — it’s doing its job.

If it keeps you watching interest rates with anxiety, the cost is higher than it looks.

Choosing wisely now protects more than your money.

It protects your peace.

Disclaimer: This content is for general informational purposes only and does not replace personalized financial advice. Consider speaking with a qualified professional before choosing a mortgage.

Selina Milani is a personal finance writer focused on clear, practical guidance on money, taxes, insurance, and investing. She simplifies complex decisions with research-backed insights, calm clarity, and real-world accuracy.

Pingback: How to Choose the Right Mortgage Type — The Calm, Confident Guide That Protects Your Money for Decades