“The Vet Visit That Changes How You See Money”

Almost every pet owner remembers that moment.

A routine visit turns complicated.

Tests are recommended.

Treatment options expand quickly.

Suddenly, the focus shifts—not from love or care—but from numbers.

In my experience working with households on financial planning and insurance decisions, pet-related expenses are among the most emotionally charged costs people face. Not because they’re frequent—but because they’re unexpected.

This is where pet insurance quietly changes the math.

Not dramatically.

Not loudly.

But meaningfully.

Why Pet Care Costs Feel Different From Other Expenses

Most household costs are predictable.

Rent.

Utilities.

Groceries.

Veterinary care is different.

Costs are:

- Irregular

- Unplanned

- Often urgent

- Emotionally sensitive

This combination makes rational decision-making harder.

When pet insurance is absent, owners often feel pressure to choose between financial comfort and medical thoroughness—even when both feel equally important.

Insurance doesn’t remove responsibility.

It removes surprise.

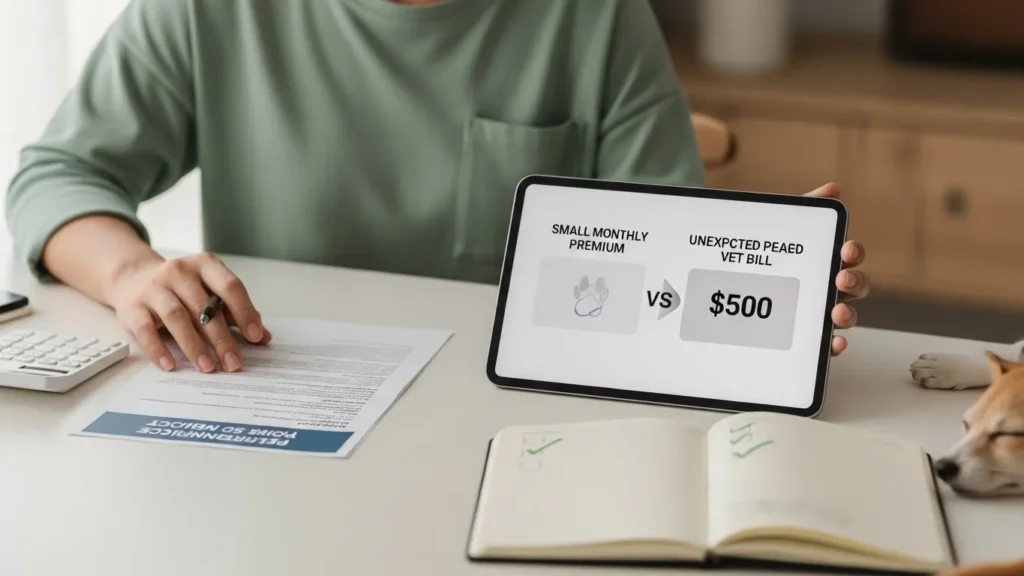

The Hidden Cost Most People Forget to Count

When people calculate pet insurance value, they usually compare:

- Monthly premiums

vs - Average annual vet visits

This misses the real financial impact.

The true cost includes:

- Emergency diagnostics

- Advanced imaging

- Surgery

- Hospitalization

- Follow-up care

These expenses don’t arrive gradually.

They arrive all at once.

Pet insurance spreads risk over time, which is why the savings often feel invisible—until a serious issue appears.

Why “I’ll Just Pay Out of Pocket” Often Backfires

Many responsible owners plan to self-fund pet care.

The intention is reasonable:

“I’ll save and pay when needed.”

The problem is timing.

Medical events rarely wait until savings are fully built.

I’ve seen situations where:

- Owners had partial savings, but not enough

- Credit was used under stress

- Treatment decisions were rushed

Insurance doesn’t eliminate costs—but it reshapes how and when they’re felt.

The Power of Risk Pooling (Without the Jargon)

At its core, insurance works by sharing risk.

Many people pay small amounts so that:

- The few who face large costs aren’t overwhelmed

- Individual events don’t become financial crises

With pets, this structure is especially valuable because:

- Costs are unpredictable

- Conditions can escalate quickly

- Emotional stakes are high

This is why the savings from pet insurance often show up in one major moment—not across every year.

A Simple Comparison: With vs Without Pet Insurance

| Without Pet Insurance | With Pet Insurance |

|---|---|

| Large, sudden expenses | Predictable monthly cost |

| Stress-driven decisions | Calmer treatment choices |

| Cash flow disruption | Financial buffering |

| Reactive budgeting | Planned risk management |

| Emotional pressure | Reduced financial strain |

The difference isn’t just financial—it’s psychological.

Why Pet Insurance Changes Decision Quality

One overlooked benefit is how insurance affects choices, not just costs.

When coverage exists:

- Owners are more likely to approve diagnostics

- Preventive care is less delayed

- Decisions are based on care quality, not affordability

This doesn’t mean “doing everything.”

It means choosing without panic.

In financial planning, this is called reducing decision stress—and it has real value.

Common Misconceptions That Skew the Math

Some beliefs quietly discourage pet insurance—even when it might help.

Common ones include:

- “My pet is young, so I don’t need it yet”

- “I’ve never had a big vet bill”

- “Insurance companies don’t pay anyway”

The reality is more nuanced.

Insurance is least expensive when risk is lower—and most valuable when risk appears unexpectedly.

Waiting until after a diagnosis usually removes eligibility for coverage of that condition.

Why Premiums Feel Larger Than They Are

Monthly premiums are visible.

Emergency bills are hypothetical—until they aren’t.

Behavioral finance shows that people:

- Overweight visible costs

- Underestimate low-probability, high-impact events

Pet insurance feels expensive because it’s predictable.

Vet emergencies feel shocking because they’re not.

This mismatch explains why many owners only appreciate insurance after the first major claim.

How Pet Insurance Often Saves Money Indirectly

Beyond reimbursements, insurance can reduce costs in quieter ways.

For example:

- Earlier diagnosis can prevent complications

- Timely treatment may reduce long-term care

- Fewer last-minute decisions avoid premium pricing

These savings don’t show up on statements—but they influence total spending over a pet’s lifetime.

What Pet Insurance Is Not

Clarity matters.

Pet insurance is not:

- A guarantee of zero expenses

- A replacement for routine budgeting

- Identical across all providers

It works best as a financial shock absorber, not a magic solution.

Understanding this prevents disappointment and improves satisfaction.

Common Mistakes Pet Owners Make With Insurance

Even well-intentioned owners can misjudge coverage.

Common errors include:

- Choosing based on price alone

- Ignoring deductibles and limits

- Not understanding reimbursement structure

- Delaying enrollment too long

A calm review before enrollment avoids confusion later.

Why This Matters More Than Ever

Veterinary medicine has advanced rapidly.

That’s good news for care.

But advanced care often means higher costs.

As options expand, so does the financial complexity of pet ownership.

Pet insurance helps align modern medical capability with financial preparedness—without forcing rushed compromises.

Practical Ways to Decide If Pet Insurance Makes Sense

Instead of asking, “Will I save money every year?”

Ask:

- Could I comfortably handle a $3,000–$7,000 surprise expense?

- Would financial pressure affect my decisions?

- Do I prefer predictable costs over rare, large ones?

The answers matter more than averages.

Key Takeaways

- Pet insurance spreads unpredictable risk over time

- Savings often appear during one major event, not annually

- Insurance improves decision quality under stress

- Emotional and financial relief are connected

- Predictability often matters more than total cost

Pet insurance doesn’t change how much you care—it changes how calmly you can act when care is needed.

Frequently Asked Questions

1. Does pet insurance always save money?

Not every year. Its value often appears during unexpected or major medical events.

2. Is pet insurance only useful for emergencies?

Emergencies highlight its impact, but it can also support ongoing care decisions.

3. Should insurance be purchased early?

Earlier enrollment often means broader eligibility and lower premiums.

4. Can I rely on savings instead of insurance?

Some people do, but insurance helps prevent large, sudden cash flow strain.

5. Is pet insurance worth it for healthy pets?

Insurance is typically most effective when obtained before health issues appear.

A Calm Conclusion

Pet insurance isn’t about expecting the worst.

It’s about removing financial shock from moments that already carry emotion.

When the unexpected happens, the quiet value of insurance becomes clear—not because it eliminates cost, but because it preserves choice.

And in those moments, that difference often matters more than the numbers.

Disclaimer: This article is for educational purposes only and reflects general financial and insurance concepts, not personalized advice.

Selina Milani is a personal finance writer focused on clear, practical guidance on money, taxes, insurance, and investing. She simplifies complex decisions with research-backed insights, calm clarity, and real-world accuracy.